Health insurance is a contract in which an insurer agrees to cover, or reimburse, eligible medical expenses on your behalf, in exchange for a premium payment that you pay periodically (monthly, yearly, or for multiple years). It serves as a financial safety net that protects you from large, unpredictable hospital bills. So, in simple terms, health insurance is the insurance taken out to cover the cost of medical care, and the ‘health insurance policy’ is a contract between an insurer and an individual/group.

When you buy a policy, you choose a sum insured, which is the maximum amount the insurer can pay in a policy year. If you’re hospitalised, the insurer covers eligible expenses up to that limit, subject to the policy’s terms and conditions. And that last part matters, because two people with the same ₹10 lakh cover can walk out of the same hospital with very different out-of-pocket costs.

This guide explains what health insurance covers, how it works in real life, the main types of health plans in India, and what you should actually look for before buying one.

What Does a Health Insurance Policy Cover?

At its core, health insurance is designed to cover medically necessary hospitalization.

That typically includes the cost of staying in the hospital or room rent, doctor and surgeon fees, ICU charges, medicines, diagnostics, and treatment-related expenses. Most comprehensive plans also extend coverage to expenses incurred just before admission, like tests and consultations, and for a defined period after discharge, such as follow-up visits and medicines.

Over the years, insurers have expanded coverage to include day-care procedures that don’t require a 24-hour admission, ambulance costs up to a limit, domiciliary treatment in specific situations, alternative (AYUSH) treatments or hospitalization, wellness and preventive care, and certain modern treatments recognized by IRDAI.

But it’s important to keep expectations grounded. Health insurance is primarily about paying hospital bills. Everything beyond that depends on the policy wording. That’s why two plans with similar premiums can behave very differently at claim time.

Refer to our Health Insurance Checklist to get an idea about what to expect from a decent health insurance policy.

How Does Health Insurance Work?

Health insurance works by helping you manage medical costs through a shared-risk system between you and the insurer. Here’s a step-by-step explanation on what is health insurance capable of and how it works for policyholders.

For a more detailed understanding, you can check our guide on How Health Insurance Works.

Talk to an expert

today and

find

the right

insurance for you.

Types of Health Insurance

IRDAI broadly classifies health insurance into two types: Indemnity-based, which reimburses your actual hospital expenses (up to the sum insured), and Benefit-based, which pays a fixed lump sum on occurrence of a covered event like a critical illness diagnosis, regardless of the bill amount.

In India, health insurance is treated as a non-life (general) insurance line. Health policies are offered by general insurers and standalone health insurers. They broadly fall into the following categories:

Common Health Insurance Categories

Can You Take Multiple Health Insurance Policies?

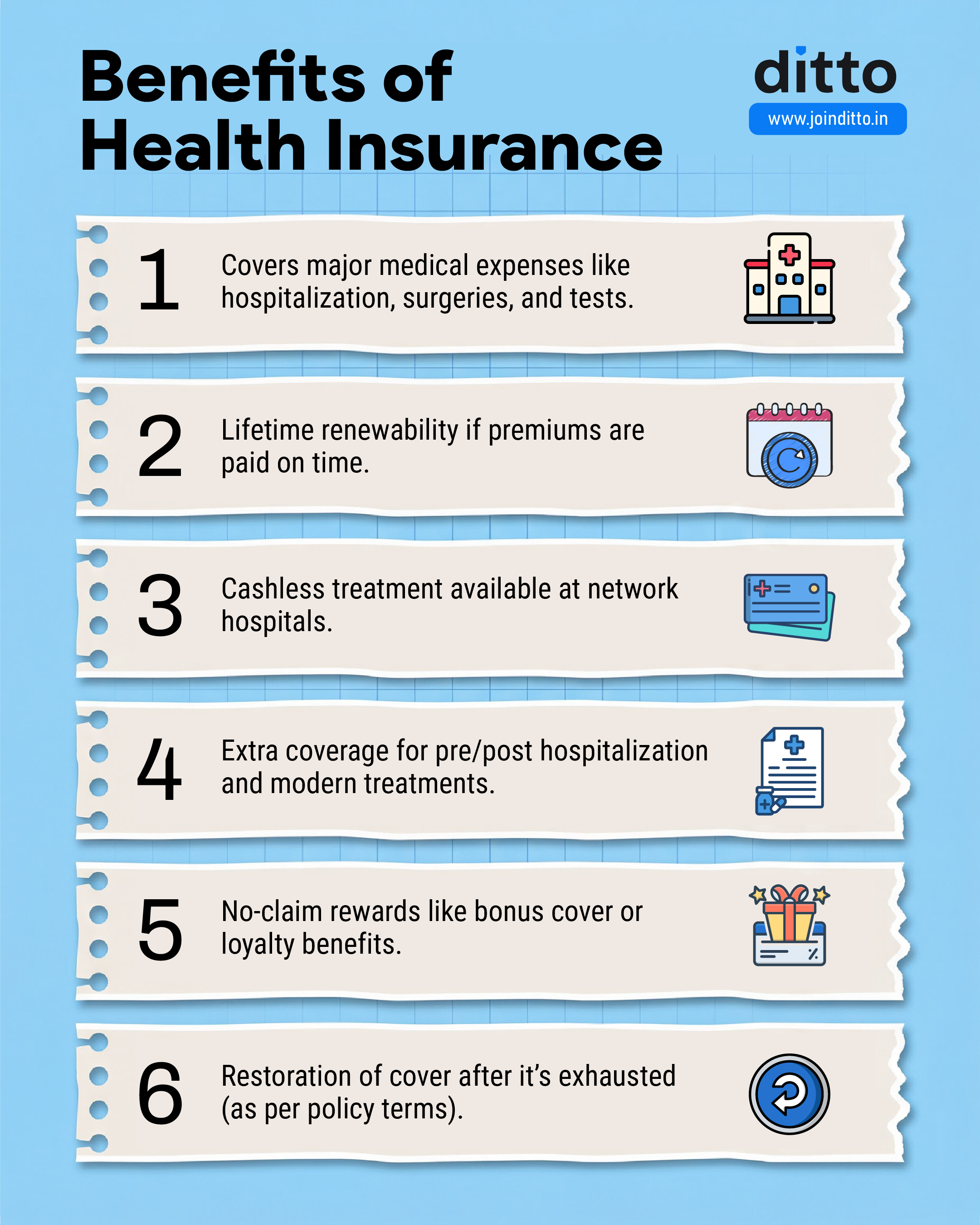

Benefits of Health Insurance

Health insurance combats medical inflation by covering hospitalization, surgeries, and diagnostics, generally up to the sum insured. The following infographic provides an overview of the overall benefits of health insurance:

What Is Not Covered Under Health Insurance?

No policy ever covers conditions or treatments under the permanent exclusions in health insurance. Examples include congenital anomalies (only internal), non-medical and investigative procedures, and OPD and maternity (unless specifically stated as covered), and injuries due to war, civil unrest, or nuclear radiation.

Always review the exclusions section carefully. Many claim disputes arise from assumptions rather than mis-selling.

Quick Note: The most common permanent exclusion is claims due to substance abuse or anything related to smoking or drinking.

How to Choose the Right Kind of Health Insurance For Yourself?

To choose health insurance wisely, consider your age, existing health conditions, and family composition. Evaluate the type of plan, sum insured, waiting periods, exclusions, and co-payment terms. Ensure the insurer has a strong network of hospitals and a high claim settlement ratio. And avoid plans with sub-limits or restrictive room rent caps for better coverage value.

If you’re still wondering what is health insurance and how to pick the right plan, check out our step-by-step guide on How to Choose Health Insurance in India.

When Should You Buy Health Insurance?

Note: Health insurance premiums are not fixed and change over time. Increases usually occur due to movement into a higher age bracket, medical inflation leading insurers to revise premium charts, or a change in the policyholder’s location or address. Alternatively, insurers also reprice their policies after IRDAI approval.

Who Should Buy Health Insurance?

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or WhatsApp us, slots fill up fast!

Ditto’s Take on Health Insurance

Understanding what is health insurance goes beyond knowing its definition. It’s about recognizing how hospital bills behave and choosing a policy that performs predictably when you need it. A well-chosen health insurance policy protects your savings, supports better treatment decisions, and reduces financial stress during emergencies. And buying early, maintaining continuity, and selecting clean coverage without restrictive clauses often matter more than chasing the lowest premium.

At Ditto, we recommend buying health insurance when you’re young and healthy because you usually get more plan options, smoother underwriting (lower chances of exclusions or loadings), and you can serve waiting periods early while building continuity benefits over time.

To check out a list of Ditto’s recommended plans, refer to our guide on the Best Health Insurance Plans.

Alternatively, use our free Health Insurance Policy Comparison Tool to compare policies of your choice.

Note: For a detailed explanation of our process, partnership policy, and disclaimers, please see our Editorial Policy & Disclaimers document. Finally, this analysis is based on publicly available information and should not be treated as personalized advice.

Frequently Asked Questions

Why People Trust Ditto

Last updated on: