There is no single "best" health insurance company in India for everyone. The right choice depends on factors such as your age, medical history, location, and the insurer's overall performance. Based on Ditto's proprietary insurer rating framework, the best health insurance companies for 2026 are:

HDFC Ergo (4.99/5)

Bajaj General Insurance (4.99/5)

Aditya Birla Health Insurance (4.49/5)

Care Health Insurance (4.23/5)

Niva Bupa Health Insurance (4.23/5)

When evaluating a health insurer, pay close attention to these key metrics based on IRDAI data and insurers' public disclosures (FY 2022-25):

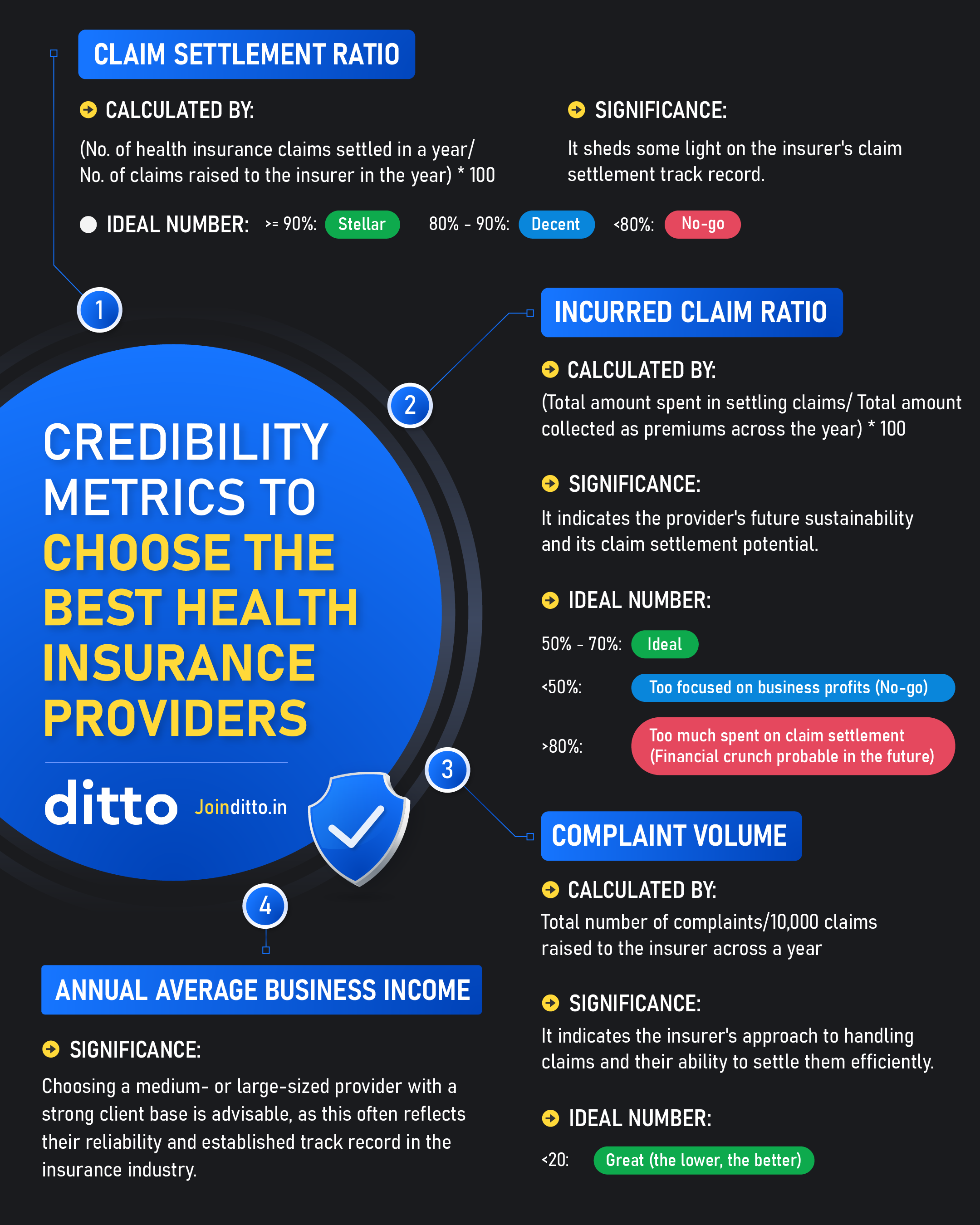

Claim Settlement Ratio (Ideal range: more than 90%, industry average: 91.22%)

Complaint Volume (Ideal range: less than 20, industry average: 27.06)

Incurred Claims Ratio (Ideal range: 50-80%, industry average: 81.88%)

Network Hospitals: Prefer insurers with at least 10,000+ cashless hospitals for wider accessibility. Also, check whether your preferred hospitals, if any, are included.

Choosing the best health insurance company in India is not just about finding the lowest premium. It is about knowing whether the insurer will support you when a medical emergency actually happens. And the numbers show why this matters.

According to the IRDAI Annual Report 2024-25, general and health insurers settled 3.26 crore health insurance claims and paid ₹94,248 crore in claim settlements. Moreover, around 87% of registered claims were settled, while about 8% were rejected and nearly 5% were still pending as of March 31, 2025.

So, before you buy a policy, it's worth looking beyond features and discounts. Let’s compare the top insurers in India based on claim settlement, complaints, hospital network, and other factors.

Note: The above metrics are for the financial years (FY) 2022-25.

Overview: Top Health Insurance Companies in India

01

HDFC Ergo

HDFC Ergo Health Insurance is one of India’s most established private insurers. It is known for its impressive claim settlement performance, financial backing, and widespread availability of cashless treatment through 16,000+ network hospitals.

HDFC

Ergo

4.99

Overall Rating

CSR Rating

5.0/5

Network Hospital Score

5.0/5

GWP Score

5.0/5

Customer Service Rating

5.0/5

Pros

Reliable insurer with strong plan structure and solid coverage options.

In-house claim servicing and a smooth digital experience.

Cons

Premiums are more expensive than peers.

02

Bajaj General

Bajaj General Health Insurance is a solid choice if hassle-free claims are your top priority. With over 12,600+ network hospitals, the insurer offers decent plans with basic features.

Bajaj

General

4.99

Overall Rating

CSR Rating

5.0/5

Network Hospital Score

5.0/5

GWP Score

5.0/5

Customer Service Rating

5.0/5

Pros

Excellent claim settlement record.

Very few complaints (lowest in the industry) and an in-house claims team.

Cons

Some plans are priced higher and may not offer as many features as competitors.

03

Aditya Birla

Aditya Birla Health Insurance has built a reputation for linking insurance with wellness by offering rewards for fitness. It also offers digital health tools and preventive-care nudges as part of its brand. Currently, it has a network of over 16,500+ hospitals.

Aditya

Birla

4.49

Overall Rating

CSR Rating

5.0/5

Network Hospital Score

5.0/5

GWP Score

3.0/5

Customer Service Rating

5.0/5

Pros

Good fit for younger buyers and families.

Attractive if you want wellness-linked premium discounts.

Cons

Relatively new compared to industry peers like HDFC Ergo or Care.

Room for improvement in customer experience because of comparatively higher complaint volumes.

04

Care Health

Care Health Insurance is one of the largest standalone health insurers. Its big draw is access: strong digital plumbing and a good cashless network 11,400+ hospitals, which makes it easier to find a tie-up hospital and get paperwork moving.

Care

Health

4.23

Overall Rating

CSR Rating

4.5/5

Network Hospital Score

3.0/5

GWP Score

5.0/5

Customer Service Rating

3.0/5

Pros

Best for cashless access across metros and tier-2/3 cities

Provides affordable policies with multiple customization options via add-ons.

Cons

Complaint volume is higher than that of peers like HDFC Ergo.

05

Niva Bupa

Niva Bupa Health Insurance consistently experiments with features, pricing, and flexibility. Its catalog is filled with innovative ideas, such as unlimited reinstatements to lock-the-clock, and often comes at competitive prices. The insurer has also partnered with 10,000+ network hospitals for cashless treatments.

Niva

Bupa

4.23

Overall Rating

CSR Rating

4.5/5

Network Hospital Score

3.0/5

GWP Score

5.0/5

Customer Service Rating

3.0/5

Pros

Offers competitively priced, comprehensive plans.

Provides benefits, such as unlimited restoration and premium lock-in.

Cons

Higher complaint volume and inconsistent claim experience.

Talk to an expert today and find the right insurance for you.

06

SBI General

SBI General Health Insurance is a subsidiary of India's largest public sector bank, State Bank of India. With 18,000+ network hospitals, the insurer is a solid mid-tier pick, especially for buyers who value brand trust.

SBI

General

3.79

Overall Rating

CSR Rating

5.0/5

Network Hospital Score

3.0/5

GWP Score

3.0/5

Customer Service Rating

3.0/5

Pros

Affordable premiums and comprehensive coverage options.

Strong and consistent claim settlement.

Cons

Complaints are still higher than those of the top-ranked insurers.

Go Digit Health Insurance is a new-age, digital-first insurer suited for buyers who are comfortable with app-first servicing and want a modern interface. Currently, it has a cashless network of 9,000+ hospitals, which is below the recommended range of 10,000+.

Go

Digit

3.7

Overall Rating

CSR Rating

5.0/5

Network Hospital Score

5.0/5

GWP Score

2.0/5

Customer Service Rating

4.0/5

Pros

Simple, paperless processes and strong claim metrics.

Suits customers who prefer speed and transparency.

Cons

Premiums are competitive and aggressively priced (not suitable in the long run).

Relatively shorter track record than established insurers.

08

Generali Central

Generali Central Health Insurance (formerly Future Generali) offers comprehensive medical plans for individuals and families. They have 10,000+ hospitals in their cashless network.

Generali Central

3.7

Overall Rating

CSR Rating

4.5/5

Network Hospital Score

1.7/5

GWP Score

3.0/5

Customer Service Rating

4.0/5

Pros

Fewer complaints and feature-rich products.

Cons

In transition phase due to the Central Bank of India’s stake acquisition.

09

ICICI Lombard

ICICI Lombard Health Insurance is one of the largest and most trusted private health insurers in India. With 11,000+ network hospitals, the insurer also has strong digital systems and a trusted brand.

Financially strong due to its scale, growth, solvency and profitability.

Cons

Inefficiencies in claim handling and customer service.

10

Tata AIG

Tata AIG Health Insurance is one of the oldest private sector insurers in the country. Despite having an excellent network of 12,000+ hospitals, it falls short when it comes to product line-up.

TATA

AIG

3.43

Overall Rating

CSR Rating

2.5/5

Network Hospital Score

3.0/5

GWP Score

3.0/5

Customer Service Rating

4.0/5

Pros

Strong brand credibility and decent plans.

Smooth customer experience.

Cons

Premiums are higher.

CSR is lower than that of industry peers like HDFC Ergo.

Sample Premiums: Best Health Insurance Companies in India

Let’s consider the sample premiums of the flagship plans of four health insurers, which are also among our top recommendations:

Profiles

HDFC Ergo Optima Secure+

Care Supreme

Aditya Birla Activ One MAX

Niva Bupa ReAssure 2.0 Platinum+

Individual Plan (Age 25)

₹13,459

₹16,294

₹10,149

₹11,271

Family Floater,2A (Ages 31 and 32)

₹21,128

₹23,153

₹16,299

₹19,176

Family Floater, 2A 1C (Ages 35, 34, and 5)

₹26,017

₹29,257

₹21,478

₹25,026

Family Floater, 2A (Ages 62 and 63)

Not available for senior citizens

₹86,069

₹66,505

₹68,239

Here, A denotes adults, and C denotes children. The premiums are calculated for individuals residing in Delhi (pin code: 110010), seeking a sum insured of ₹15 lakh. Premiums can also vary based on age, city, medical history, plan variant, and chosen add-ons.

For senior citizens, Optima Secure is a suitable alternative, as Optima Secure+ is currently unavailable beyond the plan's maximum entry-age limit of 60 years.

Top 10 Claim Settlement Ratio of Health Insurance

A claim settlement ratio, or CSR, indicates the percentage of claims an insurer successfully settles compared to the total number of claims filed. A high CSR (ideally above 90%) shows that the insurer is dependable and more likely to honor your claims quickly and efficiently.

Not every company discussed in this guide is among the top insurers with excellent CSRs.

Evaluate your personal health needs and medical history. Plans that offer comprehensive benefits for pre-existing diseases (PEDs) or include shorter waiting periods can be more suitable if you have ongoing health concerns.

02

Check All Features and Plans

Before choosing an insurer, review the range of plans and features they offer. A more comprehensive plan with fewer restrictions is usually better because it provides broader coverage and greater flexibility as your healthcare needs change over time. Look for useful features such as consumable cover, restoration benefits, no-claim bonus, daycare coverage, wellness benefits, and fewer sub-limits or disease-wise restrictions.

03

Get Expert Advice

Get advice from unbiased, advisory platforms like Ditto Insurance. This can help you shortlist plans based on your profile, and also get continued support for any changes or claims that you might make later on in your policy.

04

Understand Your Family Structure

For single folks or senior citizens with PEDs, an individual plan may suffice. However, families with multiple members, including children, may benefit more from a family floater policy that covers everyone under a single sum insured. Understanding your family’s healthcare needs helps you pick a plan that offers the right coverage and affordability.

05

Check the Insurer’s Performance Metrics

Consider the insurer’s metrics like a higher CSR (90% and above), incurred claim ratio (ICR) between 50-80%, and a network of at least 10,000+ hospitals. Do not forget to check the volume of complaints per 10,000 claims (the lower, the better) and the annual business volume.

See the infographic below to learn more about these key metrics:

How Does Ditto Choose the Best Health Insurance Companies in India?

Picking the right insurer isn’t about flashy ads or the cheapest premium. A good company should be financially sound, settle claims fairly, and make the process simple. That’s why we developed a unique insurer rating framework, i.e., a transparent, data-driven approach to evaluate every insurer.

Each insurer is evaluated across six measurable parameters, with weightages assigned based on their relative importance:

Claim Settlement Ratio (22%)

Complaint Volume (15%)

Gross Written Premium (25%)

Hospital Network (17%)

TPA Model (10%)

Online Services (10%)

Note: If you'd like to explore the detailed figures reported by insurers and the IRDAI in their annual disclosures and public reports, visit Ditto Data Labs, our proprietary repository of health insurance data, meticulously compiled, verified, and maintained by the Ditto team over the years.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Abhinav below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

There isn’t a single best health insurance company in India. Each insurer has its strengths: some excel at claim servicing, others at network coverage, and a few at product design. The right choice depends on your priorities: smoother claims, wider access, or richer features. Look for a comprehensive plan that meets all these criteria and is from an insurer with a history of solid performance.

Always compare all the options available in the market before you buy health insurance, and read the fine print carefully to avoid any surprises later. If needed, take the time to understand how different plans stack up for your specific situation so you can make a well-informed decision.

Disclaimer

We believe in full transparency around our partnerships. Our current insurer partners are HDFC Ergo, Care, Aditya Birla, Niva Bupa, ICICI Lombard, and Bajaj General. But as you can see in this list, the rankings include both partners and non-partners because the methodology is unbiased and applied uniformly across all insurers. Always speak to an IRDAI-certified advisor to find out which plans best suit your needs.

Share Your Feedback!

If you found our content helpful or have any suggestions, feel free to share your feedback with us on LinkedIn, Reddit, X, or via email at [email protected]. We'd love to hear from you!

Frequently Asked Questions

Which is the #1 health insurance in India?

HDFC Ergo is the top recommendation in this ranking because it balances claims reliability, scale, and cashless access better than most peers. It has a 4.99/5 insurer rating, a 97.61% 3-year average claim settlement ratio, and 16,000+ network hospitals. That said, there is no single no. 1 insurer for everyone. If your biggest priority is lower complaint volume, Bajaj General is just as strong, with only 3.85 complaints per 10,000 claims. The right choice depends on whether you value service, reach, or product strength most.

What are the top 5 best health insurance companies?

The top 5 health insurance companies are HDFC Ergo, Bajaj General, Aditya Birla, Care, and Niva Bupa. HDFC Ergo and Bajaj General consistently maintain a CSR above 96%. These insurers stand out for different reasons, from lower complaint volume and stronger claim settlement to wider hospital access and better product design. So while this is a good shortlist, the best pick still depends on what matters most to you.

How to choose the top 10 best health insurance company in India?

You must evaluate key metrics like CSR (ideally above 90%), a low complaint ratio, a network of 10,000+ hospitals, and your specific medical needs. For instance, if you prioritize wellness rewards, Aditya Birla’s Activ One MAX might be better, costing a 25-year-old roughly ₹10,149 for a ₹15 lakh cover. Alternatively, if you are okay with paying higher premiums for efficient, built-in benefits, HDFC Ergo is an excellent option for your needs. Always look for health insurance plans that offer comprehensive benefits for pre-existing diseases.

Which is the best health insurance company in India for family floaters?

While many claim the "no. 1" title, HDFC Ergo Optima Secure+ is a top recommendation for families due to its 3-year average CSR of 97.61%. For a family of three (ages 35, 34, and 5), the annual premium for a ₹15 lakh cover is approximately ₹26,017. In contrast, Niva Bupa offers similar cover for ₹25,026, including benefits such as in-built unlimited restorations. But choosing the right one depends on the insurer's performance and your feature preferences as well, not just premiums. Refer to our guide on family floater health insurance for more details.

Which are the top 10 best health insurance companies in India for 2026?

The top 10 best health insurance companies in India for 2026 include HDFC Ergo, Bajaj General, Aditya Birla, Care Health, Niva Bupa, SBI General, Go Digit, Generali Central, ICICI Lombard, and TATA AIG. These are ranked based on Ditto’s score, which accounts for metrics like GWP (25% weightage) and hospital network (17% weightage). For example, Care Health provides affordable customization for its 11,400+ hospital network. This is excellent because any insurer with a network of 10,000+ hospitals gives you a better chance of finding nearby cashless hospitals for treatment.

What is the claim settlement ratio of Care Health Insurance?

Care Health Insurance maintains a strong CSR of 95.45% for the FY 2024-26 period. While it is a standalone leader with over 11,400 network hospitals, its complaint volume is slightly higher at 42.67 per 10,000 claims compared to HDFC Ergo’s 8.87. For a 25-year-old, their Care Supreme plan costs about ₹16,294 for a ₹15 lakh sum insured. If you are looking for affordable policies with multiple customization options, Care Health Insurance is a solid pick.

Is Niva Bupa a good health insurance company?

Niva Bupa is excellent for those seeking flexible benefits like "lock-the-clock" and unlimited reinstatements. They have a 92.92% 3-year average CSR and a network of 10,000+ hospitals. However, they do have a higher complaint volume of 37.13 per 10,000 claims. For a family of two (ages 31 and 32), their ReAssure 2.0 Platinum+ plan costs ₹19,176 for a ₹15 lakh cover. You can read our full Niva Bupa Health Insurance review to see if it fits your needs.

What is the best health insurance company in India as per claim settlement?

If you look only at the 3-year average claim settlement ratio, Go Digit is the highest among the top 10 private insurers at 99.01%. But the claim settlement ratio alone should not decide your purchase. Scale matters too. HDFC Ergo at 97.61% and Bajaj General at 95.63% combine strong settlement numbers with annual business volumes above ₹6,500 crore, which makes their performance more meaningful over time. So the best insurer by claim settlement depends on whether you want the highest percentage alone or the strongest mix of percentage plus long-term scale.

Which health insurance company has the largest hospital network in India?

SBI General and Aditya Birla have the largest hospital networks, with 18,000+ and 16,500+ cashless hospitals, respectively. HDFC Ergo follows with 16,000+. A bigger network matters because it improves your odds of getting cashless treatment without scrambling for approvals in an emergency. That said, network size alone is not enough for most buyers. You should also check whether your preferred hospital has a tie-up with the insurer.

Can I switch my health insurance from one company to another in India?

Yes, you can port your health insurance to another insurer at renewal, retaining continuity benefits, such as credit for completed waiting periods. You should apply 30-45 days before renewal, but the new insurer will still underwrite your profile before accepting the request. Health insurance portability is useful when your current insurer has weaker claims performance, a smaller hospital network, or repeated premium hikes. Just remember that smoother portability usually depends on clean disclosures, a stable claim history, and applying on time.

Customer Reviews

4.9

20915 reviews

Ditto is doing really great. Absolutely spam free- that's the best part. They don't talk to you like they are forced to sell the product. It's more like, helping us buy better. Advisor Nuha was very patient and answered all my questions with clarity. Thanks for the service

I

INDHUMATHI M

Loved the service! Maheta Nidhi Hitesh was incredibly helpful and knowledgeable. She guided me through the whole process and made everything super easy to understand. I really appreciated how patient she was with all my questions—there was no pressure at all, just clear and honest advice. Honestly, I'm very happy with my experience at Ditto so far. Highly recommend!

RK

Ragul Kumar

I had a great experience with Ditto while exploring health insurance options. The process was smooth and everything was explained clearly.

A special thanks to Swaroop SK for patiently answering all my questions and guiding me through the policy details without any pressure. The transparency and support made it much easier to understand and choose the right plan.

Really appreciate the assistance!

PS

Pulkit Singh

Had a great experience with Ditto Insurance. Ishita Sudrania was extremely helpful in guiding me through choosing the right term plan. There was no spamming or sales pressure, and all my questions were patiently answered. She also assisted me thoroughly with the entire application process. Highly recommend!

SS

Samil Shah

I had a great experience with Ditto while filing my health insurance claim. Their team guided me clearly through the entire process, helped with the required documents, and promptly answered all my queries. Their support made the claim process much smoother and less stressful. Highly appreciate their assistance.