Health Insurance Guide

A simple guide to how health insurance actually works in real life. Let’s go!

Buying insurance feels confusing for a reason. Policy documents are long. The language is dense. And even if you try reading them, you'll probably feel lost because you won't know what half the words mean.

So this guide does one thing.

It explains how health insurance behaves at claim time, using plain language and real situations. We'll start with the basics, walk through the most important clauses that affect payouts, and end with a practical overview of how claims work.

Most people don't buy health insurance because they think they'll fall sick next month, but because they've seen what hospitals cost when something actually goes wrong. After all, a sudden admission doesn't just mean doctors and treatment, but could include ICU charges, diagnostics, medicines, room rent, and a bill that keeps growing every day you stay admitted. And at that moment, you're not just worried about health but also about money. Savings get drained, and people take loans they never planned for.

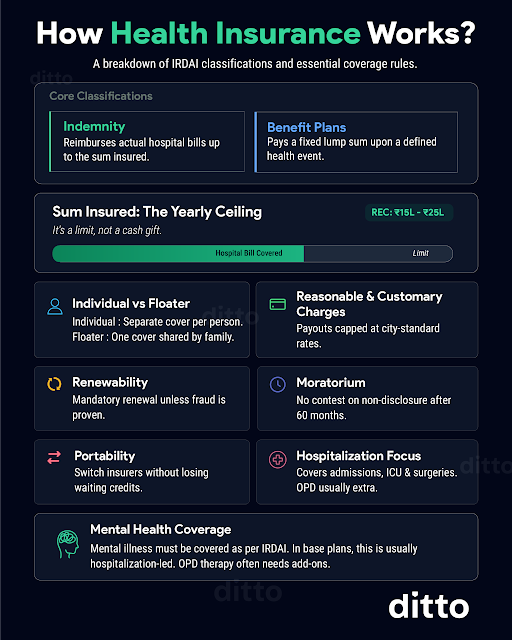

That is what health insurance is meant to prevent. You pay a premium every year. In return the insurer agrees to pay for eligible hospitalization expenses, up to a fixed limit called sum insured, and as long as the claim follows the policy rules.

Now, that last part is important. Because in real life, health insurance isn't about whether you have a policy but how that policy behaves when a claim happens. Two people can both have a "₹10 lakh cover" and walk out of the same hospital with very different settlements. And the difference usually comes down to clauses most people don't look at until it's too late.

So before we jump into clauses, let's quickly understand how health insurance is designed to work.

Now that the basics are clear, let's get into the fine print that decides how much you actually pay at discharge. We'll start with the most common clause that quietly ruins claims: co-payment.

You're about to buy health insurance. The agent pitches a ₹10 lakh cover for ₹10,000 a year, then offers a 25% discount if you accept a 20% co-payment. You save ₹2,500 a year and sign up. Nine months later, you meet with an accident, and the hospital bill comes to ₹4 lakh. The insurer pays only ₹3,20,000 and asks you to pay ₹80,000 because you agreed to co-pay 20%. You saved ₹2,500 with the clause, but paid ₹80,000, which is roughly the equivalent of 32 years of those annual savings wiped out in one claim.

That's why co-pays rarely make sense unless they're mandatory or you're buying for someone older with severe pre-existing diseases, where a co-pay can reduce premiums and sometimes improve chances of acceptance. For most first-time buyers, they create asymmetrical pain.

You already have a corporate health insurance cover, so you want an affordable personal plan as a backup. The agent offers a ₹10 lakh base policy and says you can save ₹5,000 a year if you add a ₹50,000 aggregate deductible. You agree because you assume corporate cover will take care of the first ₹50,000. Then you switch jobs or freelance, and your corporate cover ends. Two weeks later, you're hospitalized with a ₹3 lakh bill. The insurer approves the claim but makes you pay the first ₹50,000, and pays the remaining ₹2,50,000. You saved ₹5,000 but paid ₹50,000, which is roughly the value of 10 years of those premium savings, wiped out at discharge in one shot.

That's the catch: deductibles look harmless until your job changes.

Also, aggregate deductibles reset every policy year, but if it's a per-claim deductible, you pay it on every claim. Pro tip: if you take a deductible, keep that amount aside as a buffer.

Imagine falling sick and discovering your policy has a room rent cap of 1% of the sum insured. On a ₹10 lakh plan, that's ₹10,000 per day, which means you can't pick the ₹20,000 room you want. You think, "I'll be here only two days, I'll just pay the extra ₹20,000 for the room," and you go ahead anyway. Two days later at discharge, the insurer tells you to pay an extra ₹50,000. Why? Because when you choose a room above the allowed limit, insurers don't just cut the room rent, they cut other linked hospital charges in the same proportion too, like surgeon fees, consultant charges, diagnostics, and more. In your case, since the eligible room rent was ₹10,000 but you chose ₹20,000, they cover only 50% across the total bill. This is called proportionate deduction.

The simple rule: avoid room rent caps. If you must take one, a category limit like single private AC is usually better than a 1% cap, and always pick a room well within the limit.

You're offered a ₹10 lakh cover for ₹6,000 a year. It feels too good to be true, but you buy it anyway. Then a slipped disk lands you in the hospital, the surgery bill is ₹4,36,000, and the insurer agrees to pay only ₹2,00,000.

Why?

Disease wise sub-limits. The policy caps payouts for specific illnesses and procedures, even if your sum insured is higher, like ₹2,50,000 for cardiovascular conditions, ₹2,75,000 for knee replacement, and ₹2,00,000 for other major surgeries.

That's how premiums are engineered and why they are so low: in many cases, they may never pay anywhere close to the full cover amount. If possible, avoid plans with disease-wise sub-limits altogether.

The scariest part of buying insurance begins after the sweet talk ends: the insurer asks about your medical history, may order tests, and then tells you what will be covered immediately versus what will be covered only after a waiting period. If a hospitalization is linked to a pre-existing condition, you may have to wait 2 to 3 years, which can be brutal. Say you disclose high blood pressure and buy a policy, but the next year you have a heart attack, the insurer can deny the claim if they link it to the earlier condition, and you're still in the waiting period.

Most policies have a 30-day initial waiting period (only accidents are covered), a 2-year wait for specific listed conditions like cataract, hernia, knee replacement, etc, and a 3-year wait for pre-existing diseases and related complications.

So choose a plan that makes you wait the least, and consider waiting-period reduction add-ons if you think you'll need the cover sooner.

You wake up dizzy, visit your doctor, and she orders a blood test, nothing alarming, so you go home with an ORS pack. The next day, you feel worse, she orders an MRI, and after seeing the results, she asks you to get admitted. You spend three days in the hospital and get discharged, with a hospital bill of ₹50,000, plus ₹20,000 in MRIs and tests done before admission. You expect insurance to cover everything, but the insurer says pre-hospitalization expenses are not covered, meaning the costs leading up to hospitalization come out of your pocket, which is ironic because diagnostic tests before admission (and follow-ups after discharge) are often a big part of the spend.

That's why it's smart to pick a policy that covers both pre and post-hospitalization. As a baseline, look for at least 30 days pre and 60 days post, more if possible, so you're covered for tests, medicines, physiotherapy, and follow-up consultations.

You get admitted for a minor surgery, everything goes smoothly, and the hospital hands you a final bill of ₹1,40,000. You're relieved because you have insurance, so you expect a clean cashless settlement. But at discharge, the insurer approves only ₹1,28,000 and asks you to pay the remaining ₹12,000. You're confused because nothing big was rejected. Then you see the line items: gloves, masks, syringes, gauze, sutures, antiseptics, nebulization kits, oxygen masks, and a bunch of other "small" things the hospital grouped under consumables.

Many policies cap consumables or treat them as non-payables, so even in a cashless claim, the hospital can ask you to pay them at discharge. And they're not tiny; consumables can easily be 10–15% of the hospital bill. So pick a policy that covers consumables by default (or via an inbuilt add-on) and ask for a deduction sheet at discharge.

Insurers want you to stay fit, and they even reward you for it through a no-claim or loyalty bonus. For instance, some plans increase your cover above the sum insured by 50% for every claim-free year. Start with ₹10 lakh, and you could be at ₹15 lakh after one claim-free year and ₹20 lakh after the next, though most policies cap this growth at some point, often once the cover doubles. And if you make a claim later, they may claw back the bonus by the same fixed percentage.

It's still a useful feature, but only if it's meaningful. Anything below 10% is usually more marketing than value. Also, newer plans offer a loyalty-style bonus that grows with renewals, even if you make claims, up to a maximum limit, with higher caps occasionally going up to 500%, so try to pick a bonus that actually moves the needle and is not wiped out after one claim.

Talk to an expert today and

find the right insurance

for you.

It's a Sunday morning, and you're sipping coffee on a hospital bed, thinking about how a heart complication led to a 3-week stay and a bill of ₹8,88,000. Thankfully, you have a ₹10 lakh cover, so you don't have to pay anything. But then it hits you: this is a floater policy with your wife, and you've used up most of the sum insured, so if she needs hospitalization soon, the remaining cover may not be enough.

Now imagine the insurer refills your cover and gives you another ₹10 lakh for the same policy year. That's exactly what a restoration benefit can do. Some plans offer unlimited restoration, while others add restrictions, like not allowing restoration for the same illness again, such as another heart-related claim.

That's why restoration is worth having, especially in floaters (and even in individual plans), but you should always read the fine print on when it triggers and how it restores.

Say you go through an appendicitis surgery and are discharged the same day. The procedure is done, you're out within 24 hours, and the bill is ₹80,000. You call your insurer expecting full coverage, but they say it isn't covered because your policy excludes daycare treatments, meaning procedures that need hospital infrastructure but get completed within 24 hours, like chemotherapy, dialysis, or even an appendectomy.

In reality, because of IRDAI-driven standardization, most retail plans today do cover daycare procedures, but the cover is often restricted to a listed set of procedures and subject to terms and conditions. So, always check the policy wording carefully!

You wake up with a bad cold that quickly turns into nonstop coughing and breathing trouble. You call the hospital, but they say there are no beds. Your only option is treatment at home, and it's going to cost a lot, until your insurer tells you they'll cover it because you're being treated at home due to a medical or logistical reason. It's rare to be in that spot, but you're glad the benefit exists.

Domiciliary cover is a good-to-have, and in most cases, you don't need to hunt for it because many retail health plans include it by default, subject to conditions like a minimum duration (often 72 hours), a doctor's certification of medical necessity, and a valid reason such as no beds being available or the patient not being fit to be moved.

A full-body health checkup usually costs ₹2,000 to ₹4,000, which adds up if you do it regularly.

This is why some insurers offer free health checkups, maybe every year, maybe once in two years, as a small bonus. It's nice to have, but not a deal-breaker, because the benefit is often restrictive: there may be a low cap, only a fixed list of tests, and only at partner centres. So treat it as a good-to-have, not the deciding factor while choosing a plan.

Still unsure about co-payments, room rent limits, or which add-ons actually matter? You're not alone, and you don't have to figure it all out by yourself.

Join our FREE 90-minute masterclass where our IRDAI-certified experts will break down everything in simple, clear terms - no jargon. Register now so you can make better informed decisions!

You're pushing 50, and you've been feeling breathless for weeks, but one evening it gets bad enough that you visit your doctor. He suggests an invasive procedure next, but you're not comfortable, so you decide to try traditional treatment first and go to an AYUSH (Ayurveda, Yoga, and Naturopathy, Unani, Siddha, and Homoeopathy) hospital. The practitioner examines you, admits you for three nights, and the bill comes to ₹75,000, which makes you wonder if health insurance will even cover AYUSH.

IRDAI has pushed insurers to treat AYUSH at par with other treatments and remove restrictive limitations. But there's a catch: this is meant for medically necessary inpatient treatment, not preventive or rejuvenation packages, so a wellness retreat or a "just to feel better" Panchakarma plan won't qualify. Also, AYUSH claims can be trickier in practice: cashless usually works only if the AYUSH hospital is in the insurer's network, so many claims become reimbursement, and eligibility often depends on factors like 24+ hours of admission and treatment at a recognized, accredited AYUSH facility.

You're thinking of having kids, so you start planning for childbirth, especially the hospitalization bill, and you wonder if health insurance can offset that cost. It sounds like a solid idea, but it comes with baggage. Insurers know maternity claims are predictable, which means they will almost certainly have to pay, so many plans don't offer the benefit at all, and the ones that do make sure they price it in. That usually shows up as much higher premiums, long waiting periods, and sub-limits that cover only a part of the expense.

Sometimes the benefit is offered only on family plans, where both you and your spouse must be covered, even if only one of you will use maternity. There's no free lunch, so if you're choosing a maternity plan, make sure you're not paying ridiculously high premiums for a benefit that may not be worth it.

Most people visit a doctor at least once a year, and if your doctor charges through the roof, it's tempting to buy a plan with OPD reimbursement and call it a genius move. But alas, nothing is that simple. The insurer knows they'll almost certainly have to pay you something every year, because let's be honest, you're going to see a doctor again, and you'll pay over ₹1,000 in consultation fees sooner or later.

That's why many insurers don't offer OPD at all, and the ones that do price it in either by pushing premiums up or covering only a small part of the expense.

The catch is that OPD cover often looks like savings, but comes back as a higher premium, so before you buy it, do a basic check: compare the extra premium you'll pay versus the OPD amount you'll realistically claim each year. In many cases, paying OPD out of pocket is cheaper.

If you remember one thing, make it this: health insurance is only as good as its fine print at claim time. A policy can look "cheap" for years, then punish you at discharge through co-pays, sub-limits, room rent deductions, and consumables.

So our advice is boring:

Buy a clean, comprehensive base policy early, renew it on time, and don't optimize for premium.

Your non-negotiables:

- Fewer payout traps: avoid room rent caps, disease-wise sub-limits, and forced co-pays unless unavoidable.

- Lower "discharge-time surprises": check consumables/non-payables handling, and watch for "reasonable and customary" deductions.

- Continuity matters: renew without breaks so waiting periods and credits stay protected.

- Know your escape hatches: if your plan turns out to be annoying, you can migrate within the same insurer or port to another insurer while carrying key credits (waiting periods, accumulated bonus, and even moratorium credit), subject to underwriting by the new insurer.

Health insurance works best when it’s bought calmly, understood early, and never rushed during a crisis.

If you’re unsure which plan to pick or what the fine print actually means for your situation, speak to a Ditto advisor. We’ll help you evaluate plans, explain the trade-offs, and stay with you during claims if you need us.

with a Ditto advisor or .